VFIAX vs VOO: Which Vanguard S&P 500 Fund Should You Choose?

VFIAX vs VOO is one of the most common investing questions. This guide breaks down expense ratios, minimums, tax treatment, and trading differences so you can pick the right fund for your situation.

This post is for informational purposes only and does not constitute financial advice. Consult a qualified financial advisor before making investment decisions.

If you have been trying to decide between VFIAX vs VOO and keep reading that they are “basically the same thing,” that is true, but it leaves out the details that actually matter for your specific situation. Both are Vanguard S&P 500 funds. They track the same index, hold the same stocks, and deliver nearly identical returns. The difference is structural, and that structure changes how you invest, how you get taxed, and which one fits your account setup. This guide covers all of it without unnecessary complexity.

What Are VFIAX and VOO?

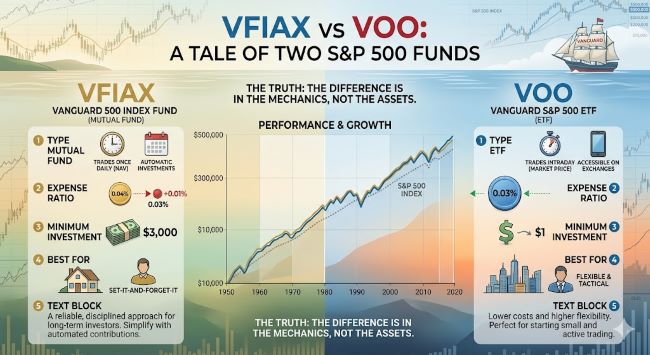

VFIAX is the Vanguard 500 Index Fund Admiral Shares, a mutual fund that has been around since 1976, making it one of the oldest index funds available to individual investors. It tracks the S&P 500 and carries an expense ratio of 0.04%. It requires a $3,000 minimum initial investment and trades once per day at the end of market hours at its net asset value (NAV).

VOO is the Vanguard S&P 500 ETF, launched in 2010. It tracks the same S&P 500 index and carries a slightly lower expense ratio of 0.03%. There is no minimum investment beyond the cost of one share, which sits around $540 as of mid-2025. It trades throughout the day on an exchange like any stock.

Here is the key fact that simplifies everything: VFIAX and VOO are technically two share classes of the same underlying fund. They hold the same securities in the same proportions. The performance difference over a decade is about 0.05% annualized, which comes entirely from the fee gap.

VFIAX vs VOO: Head-to-Head Comparison

| Feature | VFIAX | VOO |

|---|---|---|

| Fund type | Mutual fund | ETF |

| Expense ratio | 0.04% | 0.03% |

| Minimum investment | $3,000 | ~$1 (fractional) or ~$540 (full share) |

| Trading | End of day at NAV | Intraday like a stock |

| Automatic investing | Yes, natively | Manual or broker-dependent |

| Dividend yield (TTM) | ~1.08% | ~1.08% |

| 10-year annualized return | ~15.09% | ~15.14% |

| Tax efficiency | Good, but slightly behind ETFs | Slightly better in taxable accounts |

Is VOO a Mutual Fund?

This comes up often. The short answer is no. VOO is an ETF, not a mutual fund. It trades on an exchange during market hours, has a bid-ask spread, and is priced in real time rather than at the end of the day.

VFIAX is the mutual fund version. It prices once per day, and you buy or sell at whatever the NAV is at market close, regardless of when you submit the order.

The confusion happens because Vanguard uses a unique structure where many of its ETFs are legally share classes of an existing mutual fund. VOO and VFIAX share the same underlying pool of assets, which is why they have identical holdings and nearly identical performance. But the mechanics of buying, selling, and taxing them are different.

VFIAX Expense Ratio: Does the 0.01% Difference Matter?

The VFIAX expense ratio is 0.04% per year. VOO’s is 0.03%. That is a one basis point difference.

On a $10,000 investment, that costs you $1 extra per year in VFIAX. On $100,000, it is $10 per year. Compounded over 30 years at 8% annual returns, the research shows a cumulative difference of roughly $1,830 in favor of VOO on a $100,000 investment. That is real money, but it is also less than 0.3% of your final portfolio value over three decades.

The point is not that fees do not matter. They do, and compounding works against you over time. The point is that for most investors, the 0.01% gap between these two specific funds is not the deciding factor. The structure, access, and account type matter more than the fee difference when choosing between these two.

VFIAX Stock: Is VFIAX a Stock?

VFIAX is not a stock. It is a mutual fund. The term “VFIAX stock” sometimes appears in search queries, but what people usually mean is the current price or performance of the fund.

Unlike stocks, VFIAX does not trade on an exchange. You cannot buy it through most brokerages outside of Vanguard’s platform, and it does not have a real-time price that fluctuates throughout the trading day. You submit a purchase order and receive shares at the NAV calculated after market close.

VOO, on the other hand, does trade like a stock. It has a ticker symbol on NYSE Arca, an intraday price, and a bid-ask spread. You can place market orders, limit orders, or stop orders just like you would with any equity.

VTSAX vs VOO: Where Does VTSAX Fit In?

If you have seen the VTSAX vs VOO debate, it is worth addressing because it often comes up alongside the VFIAX comparison.

VTSAX is Vanguard’s Total Stock Market Index Fund Admiral Shares. The difference from VFIAX and VOO is the index it tracks. VFIAX and VOO track the S&P 500, which covers roughly 500 large-cap U.S. companies. VTSAX tracks the entire U.S. stock market, including mid-cap and small-cap companies, for a total of around 3,700 stocks.

In practice, VTSAX and VFIAX or VOO have moved very closely over time because large-cap stocks dominate market cap-weighted indexes. But VTSAX gives you broader diversification across company sizes. The expense ratio for VTSAX is also 0.04%, the same as VFIAX.

The VTSAX vs VOO decision comes down to whether you want pure large-cap S&P 500 exposure or the full U.S. market. Neither is wrong. It depends on your preference for breadth.

Tax Differences: Where VOO Has a Real Edge

In a tax-advantaged account like a 401(k), IRA, or Roth IRA, tax treatment does not affect your returns directly. In that case, VFIAX and VOO are interchangeable.

In a taxable brokerage account, the story is slightly different. Most ETFs, including VOO, use in-kind redemption mechanisms to avoid distributing capital gains to shareholders. This means you typically only pay capital gains tax when you sell your own shares, not when other investors in the fund trigger a sale.

Mutual funds, including VFIAX, can sometimes distribute capital gains to all shareholders at year-end, even if you did nothing. Vanguard’s unique share class structure reduces this risk significantly for VFIAX compared to most mutual funds, but it does not eliminate it entirely. For long-term taxable investors who are tax-sensitive, VOO has a slight structural edge.

Which One Should You Choose?

The decision is less about which fund is “better” and more about which structure fits your situation.

Choose VFIAX if:

- You invest through Vanguard’s own platform and want automatic monthly contributions without manual effort

- You have at least $3,000 to meet the minimum and prefer end-of-day pricing

- You like the simplicity of mutual fund investing with automatic dividend reinvestment

- You are investing inside a tax-advantaged account where tax efficiency is not a concern

Choose VOO if:

- You are starting with less than $3,000 and cannot meet VFIAX’s minimum

- You invest through a non-Vanguard brokerage, where VFIAX may not be available or may carry a transaction fee

- You are investing in a taxable account and want marginally better tax efficiency

- You want intraday flexibility, the ability to set limit orders, or prefer the ETF format

You can also convert VFIAX to VOO without a taxable event if you decide you prefer the ETF structure later. Vanguard allows a one-way conversion from VFIAX shares to VOO shares. The reverse is not available.

Practical Considerations Most People Miss

Brokerage availability matters. VOO is available at virtually any brokerage commission-free. VFIAX is primarily available through Vanguard’s own platform. If you invest at Fidelity, Schwab, or another broker, VOO is the straightforward choice.

Dollar-cost averaging is easier with VFIAX. If you want to invest exactly $500 per month, VFIAX lets you do that natively because mutual funds support fractional purchases. With VOO, you need either a broker that supports fractional ETF shares or you accept that your investment amount will vary with the share price.

The bid-ask spread with VOO is a real cost. VOO trades at around $540 per share, and the bid-ask spread is typically very tight, but it is a cost that VFIAX does not have. For frequent traders this adds up. For long-term buy-and-hold investors it is negligible.

Understanding how to track your investment performance and expenses across accounts helps you stay on top of which fund is working for you. Tools that help you monitor financial activity across your investment accounts make that process less manual, especially when you hold both types of accounts. And for anyone building broader financial literacy around where and how to invest, resources that cover investment tools and decision-making frameworks are worth having in your reading list.

Key Takeaways

- VFIAX vs VOO is not a performance question. Both track the S&P 500 and deliver essentially the same returns over time. It is a structure question.

- The VFIAX expense ratio is 0.04%. VOO is 0.03%. The one basis point difference is real but not the main deciding factor for most investors.

- Is VOO a mutual fund? No. VOO is an ETF that trades intraday. VFIAX is the mutual fund version of the same underlying Vanguard 500 fund.

- VFIAX requires a $3,000 minimum. VOO requires the price of one share, or as little as $1 at brokerages that support fractional ETF investing.

- In taxable accounts, VOO has a slight tax efficiency edge. In tax-advantaged accounts, choose whichever fits your brokerage and contribution style.

- VTSAX vs VOO: VTSAX covers the entire U.S. market including mid and small caps, while VOO covers only the S&P 500 large caps. Both are solid long-term choices.

- You can convert VFIAX to VOO tax-free at Vanguard. You cannot convert the other direction.

The bottom line: if you are at Vanguard and like automating contributions, go with VFIAX. If you are at any other brokerage or just starting out with limited capital, go with VOO. Either way, you are holding the same portfolio.