What Must an Entrepreneur Do After Creating a Business Plan: Your Next Steps

Your business plan is finished. You’ve spent weeks perfecting it, researching your market, projecting numbers, and outlining strategies. You feel accomplished. You feel ready. And then the real question hits: what must an entrepreneur do after creating a business plan? You realize the document sitting on your computer is just the beginning. The actual work of transforming your vision into a functioning business is about to start.

The temptation is strong to feel like you’ve completed the hard part. The business plan looks professional. It covers your market, your financial projections, your marketing strategy, your operational approach. Surely now comes the easy part, right? Wrong. A business plan is a collection of assumptions waiting to be tested. The real work happens when you move from planning into execution. Understanding what must an entrepreneur do after creating a business plan separates those who talk about starting a business from those who actually do it.

Validate Your Business Idea Before Investing

Most entrepreneurs skip this step. They’ve created their business plan, believe in their idea, and want to move immediately to launch. This impulse causes more business failures than almost anything else. Validating your business idea is non-negotiable before spending significant money.

Market Validation Steps:

- Interview potential customers to understand if they have the problem you’re solving

- Test core assumptions from your business plan against real market feedback

- Build a minimum viable product (MVP) rather than a fully developed solution

- Gather data on whether people will actually buy what you’re selling

- Identify weaknesses in your business plan before they become expensive problems

Market validation doesn’t mean building your entire product. It means validating that real people want your solution. Create a simple version. Show it to potential customers. Ask them directly: Would you buy this? Why or why not? Their answers matter infinitely more than your assumptions.

According to Harvard Business Review research, most startup failures don’t happen because the business plan was poorly written. They happen because the idea didn’t achieve product-market fit. Market validation tests this before you invest heavily.

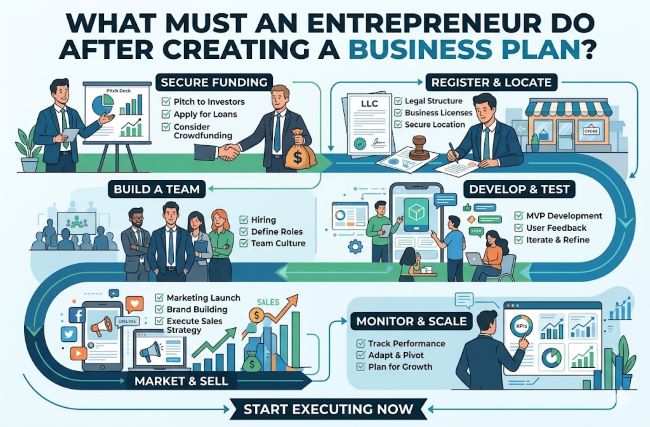

Secure Funding for Your Business

Once you’ve validated your idea, securing funding becomes critical. Even bootstrap-friendly business models require capital. You need money for equipment, inventory, hiring, marketing, and working capital to sustain you until the business becomes profitable.

Funding Options to Consider:

- Bootstrapping using your own savings and resources to maintain full control

- Friends and family funding from trusted people who believe in you

- Bank loans and SBA loans from traditional financial institutions

- Crowdfunding platforms where many people contribute small amounts

- Angel investors wealthy individuals seeking startups with high growth potential

- Venture capital for startups pursuing explosive scaling

Before approaching any funding source, clarify your numbers. How much money do you actually need? Where will it go? When will you be profitable? Your business plan should answer these questions, but be prepared to discuss them in detail.

Investors and lenders use your business plan as a starting point, but they want to see more. They want to understand your unique selling proposition. They want to know why your business will succeed when others fail. They want evidence of market validation. They want to see your team.

Register Your Business Legally

You can’t operate legally without completing essential legal steps. This includes choosing your business structure, registering your business name, obtaining an Employer Identification Number (EIN), and securing necessary licenses and permits.

Legal Registration Requirements:

- Choose a business structure like sole proprietorship, partnership, LLC, or corporation

- Register your business name with your local or national business authority

- Obtain an EIN (Employer Identification Number) from the IRS

- Register for state and local taxes based on your business type

- Apply for business licenses and permits specific to your industry

- Open a business bank account to separate personal and business finances

Each business structure has different implications for taxes, liability, and operations. Most first-time entrepreneurs choose an LLC because it balances protection and simplicity. Filing paperwork isn’t glamorous. It doesn’t directly generate revenue. But skipping it creates legal liability and operational complications you’ll regret.

Protect Your Intellectual Property

Before launch, protect what makes your business unique. This might include trademarks for your brand name and logo, patents for your product design, or copyrights for your creative content.

Intellectual Property Protection:

- Trademark your brand name and logo to protect your brand identity

- Patent your unique product or process if applicable

- Copyright your creative content like books, videos, or artwork

- Register your domain name for your website

- Document your trade secrets and keep them confidential

- Create operating agreements to protect internal processes

Understanding the differences between trademarks, copyrights, and patents is critical. Each protects different intellectual property types. Trademarks protect brand assets. Copyrights protect creative works. Patents protect inventions. Professional intellectual property guidance is often worth the investment here.

Build Your Brand and Marketing Strategy

Your business plan outlined marketing concepts. Now you implement them. Building your brand goes far deeper than your logo and business name. Brand represents customer perception, positioning, and the promise you make to customers.

Brand Building Elements:

- Define your unique value proposition that differentiates you from competitors

- Establish brand identity including name, logo, and visual elements

- Develop brand messaging that clearly communicates your promise

- Create brand guidelines for consistent representation everywhere

- Build brand authority through quality products and customer service

- Establish your online presence across relevant platforms

Marketing strategy becomes actionable now. You’ve researched your target audience. You understand their needs. Now create marketing content that reaches them. This might be social media posts, blog articles, email campaigns, advertising, or video content.

Successful entrepreneurs conduct continuous market research throughout this phase. Markets shift. Competitors respond. Customer preferences evolve. Your marketing strategy must adapt to these realities rather than rigidly following your business plan.

Assemble Your Team

No entrepreneur succeeds alone. Building your initial team is critical. You might start with just yourself and a co-founder. You might hire employees, contractors, or advisors. Regardless, assembling people who fill your blind spots accelerates growth exponentially.

Team Building Priorities:

- Identify skill gaps you need to fill with team members

- Define clear job descriptions for each role

- Recruit talent with skills different from your own

- Develop training systems so team members understand your vision

- Establish clear roles and responsibilities to avoid confusion

- Build company culture that attracts and retains good people

Most founders hire people like themselves. This is a mistake. You need people who complement your skills, not duplicate them. If you’re creative, hire detailed-oriented people. If you’re strategic, hire implementers. Diverse teams outperform homogeneous ones consistently.

Set Up Operations

Your business plan outlined your operational approach. Now you execute it. Whether you need physical space, equipment, suppliers, or software systems, operational setup ensures you can deliver value to customers consistently.

Operational Setup Tasks:

- Secure physical location if needed for your business model

- Procure equipment and supplies required for your operations

- Establish supplier relationships to ensure reliable inventory or materials

- Create processes and procedures for consistent service delivery

- Set up accounting systems to track finances accurately

- Implement project management tools to organize your work

Operational discipline separates scalable businesses from chaotic ones. You might know your product inside and out, but if your processes are disorganized, customer experience suffers. If your accounting is sloppy, you can’t make good financial decisions. If your supplier relationships are weak, you’ll face constant disruptions.

Execute Your Launch Strategy

Launch day arrives. You’ve validated your idea. You’ve secured funding. You’ve registered legally. You’ve protected your intellectual property. You’ve built your team. You’ve set up operations. Now comes the exciting part: launching your business.

Pre-Launch Marketing:

- Create pre-launch buzz through social media, email, and word-of-mouth

- Generate anticipation with early access or special offers

- Build email list of interested customers

- Establish partnerships with complementary businesses

- Prepare customer service systems for incoming inquiries

- Have a launch day checklist to manage details

Your launch day doesn’t determine success, but it creates momentum. Strong launches build social proof. Social proof builds trust. Trust converts customers. But launch is not the finish line. It’s the starting line.

Measure Performance and Adapt

After launch, your business plan becomes a living document. Measurement and adaptation separate successful founders from struggling ones.

Post-Launch Measurement:

- Track key performance indicators (KPIs) relevant to your business

- Monitor cash flow weekly to understand your financial health

- Gather customer feedback through surveys and conversations

- Analyze what’s working and what needs adjustment

- Review competitive landscape for emerging threats

- Pivot or iterate based on real market data

Many entrepreneurs make the mistake of becoming married to their business plan. Markets change. Customers reveal unexpected preferences. Competitors make unexpected moves. Your ability to measure reality and adapt quickly determines long-term success far more than the quality of your initial plan.

Key Takeaways

- What must an entrepreneur do after creating a business plan starts with validating your business idea through real customer feedback, not assumptions.

- Securing funding comes after validation, ensuring you’re investing money in an idea that actually resonates with customers.

- Legal registration is non-negotiable and includes choosing your business structure, registering your name, obtaining your EIN, and securing necessary licenses.

- Intellectual property protection prevents competitors from stealing your unique assets and is ideally completed before launch.

- Building your brand and implementing your marketing strategy operationalizes the concepts from your business plan into real customer engagement.

- Assembling your team with complementary skills accelerates growth and fills blind spots you can’t solve alone.

- Setting up operations with clear processes, equipment, and supplier relationships ensures consistent service delivery.

- Executing your launch with momentum and preparation generates initial customer traction and social proof.

- Measuring performance and adapting is ongoing work that separates successful founders from struggling ones.

Related Resources

Building a successful business requires understanding both planning and execution. Learn more about business strategy and growth by exploring startup resources which covers tools for launching your business online. For those managing teams and operations, business software includes collaboration tools to keep everyone aligned. If you’re documenting your entrepreneurial journey, business blogging covers content creation for building authority.