403b vs 457b: The Complete Guide to These Two Retirement Plans

Confused about 403b vs 457b? This guide explains what each plan is, who qualifies, contribution limits, withdrawal rules, and why contributing to both is one of the best moves you can make.

This post is for informational purposes only and does not constitute financial or tax advice. Consult a qualified financial advisor or tax professional regarding your specific situation.

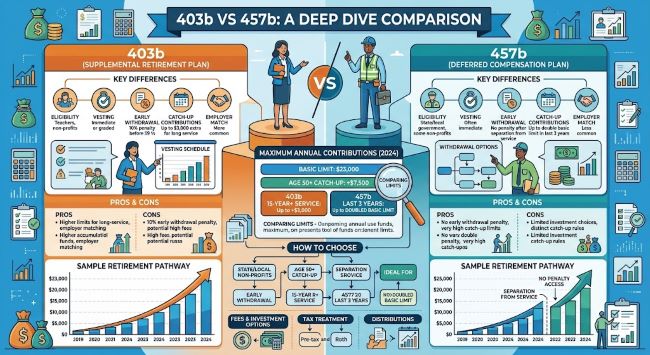

If you work in education, government, or a nonprofit and have access to a 403b vs 457b choice, you are in a genuinely good position. Both are tax-advantaged retirement accounts that most private-sector workers cannot access, and if your employer offers both, you can contribute to each one independently and effectively double your tax-deferred savings space. Most people pick one and ignore the other, or worse, ignore both and leave a lot of money on the table. This guide explains exactly what each plan is, who qualifies, how the numbers work in 2026, and when it makes sense to prioritize one over the other.

What Is a 403b Plan?

A 403b plan is a tax-advantaged retirement savings account available to employees of specific types of organizations. The name comes from Section 403(b) of the Internal Revenue Code.

Who can participate in a 403b retirement plan:

- Public school teachers and administrators at K-12 schools

- Employees of colleges and universities, both public and private

- Nonprofit hospital employees

- Employees of qualifying 501(c)(3) tax-exempt organizations

- Employees of churches and religious organizations

Historically, the 403b plan was built around annuity contracts, which is why you will sometimes hear it called a tax-sheltered annuity or TSA. Many 403b plans now offer mutual funds as well, but the annuity origin explains why some older plans carry higher fees than comparable 401(k) or 457b plans.

The 403b plan functions similarly to the more familiar 401(k). You contribute pre-tax dollars from your paycheck, reducing your taxable income for the year. The money grows tax-deferred inside the account, meaning you pay no taxes on gains, dividends, or interest until you withdraw. When you do withdraw in retirement, those withdrawals are taxed as ordinary income.

What Is a 457 Plan?

A 457b plan is a deferred compensation plan governed by Section 457(b) of the Internal Revenue Code. It comes in two versions: governmental and non-governmental.

Governmental 457b plans are offered by state and local government employers. These include city and county governments, public universities that function as government entities, public school districts, and state agencies. Governmental 457b plans offer the broadest set of features and protections.

Non-governmental 457b plans are offered by certain tax-exempt private organizations, typically for highly compensated executives and key management employees. These plans have more restrictions and are considered “top-hat” plans, meaning they are not required to be nondiscriminatory in who can participate.

When most people search for “what is a 457 plan,” they are asking about the governmental version. That is the one available to teachers, firefighters, police officers, public hospital employees, and other public sector workers. Most of this guide focuses on governmental 457b plans because they carry the most advantages.

The 457 retirement plan operates on a deferred compensation model. Like the 403b, your contributions reduce your taxable income today, and the money grows tax-deferred until withdrawal. But the 457b has some features that make it genuinely different from the 403b, particularly around early withdrawals.

Who Gets Access to Which Plan?

The decision between 403b and 457b often comes down to your employer, not your personal preference. You can only participate in a plan your employer offers.

403b plan: Available to employees of public schools, private K-12 schools, colleges and universities, qualifying nonprofits, and religious organizations. Not available to government employees who are not in education.

457b plan: Available to state and local government employees and, in the non-governmental version, certain high-earning executives at private tax-exempt organizations.

Where both plans overlap: Many public school teachers and public university employees have access to both plans simultaneously. Public school districts often offer a 403b through their nonprofit status and a 457b through their government affiliation. This overlap is where the real power is.

If you work in a public school district and your employer offers both plans, you are eligible to contribute to both in the same year, with separate contribution limits for each.

Contribution Limits for 2026

For 2026, the contribution limit for both the 403b plan and the 457b plan is $24,500 per year. These limits adjust periodically for inflation.

Age 50+ catch-up: If you are 50 or older, you can contribute an additional $8,000 per year to either or both plans, bringing the total to $32,500 per account.

Ages 60 to 63 super catch-up (SECURE 2.0): Starting in 2025, a new enhanced catch-up contribution applies to participants aged 60, 61, 62, and 63. These individuals can contribute an additional $11,250 instead of the standard $8,000, for a total of $35,750 per plan.

The key point on 403b vs 457b limits: The IRS treats these as two completely separate buckets. Your 403b contributions do not reduce your 457b contribution limit, and vice versa. This is the opposite of how 401(k) and 403b work together, where combined contributions count against a shared limit.

Practically, this means a teacher aged 55 who has access to both a 403b and a 457b can contribute $32,500 to each plan in 2026, for a combined total of $65,000 in tax-deferred retirement savings for the year. That is a significant advantage not available to most private-sector workers.

Special Catch-Up Provisions

Each plan has a unique additional catch-up option:

403b 15-year service catch-up: If you have worked for the same employer for at least 15 years and have contributed an average of $5,000 or less per year during that period, you may contribute an extra $3,000 per year, up to a lifetime maximum of $15,000. This provision is complex to calculate and very few plans implement it, but it exists.

457b near-retirement catch-up: If you are within three years of your plan’s normal retirement age, you can contribute up to double the annual limit. In 2026, that means up to $49,000 in a single year to a 457b plan. This is a significant option for people ramping up savings in the final stretch of their career.

The Biggest Difference: Early Withdrawal Rules

This is where the 403b and 457b plans diverge most noticeably, and it matters more than most people initially realize.

403b retirement plan early withdrawal rules: If you take money out of a 403b before age 59½, you pay income tax on the withdrawal plus a 10% early withdrawal penalty. There are exceptions for certain hardships, disability, and a few other situations, but the default for early access is a penalty.

457b plan early withdrawal rules: No 10% early withdrawal penalty. Ever. If you leave your government employer at any age, including at 40 or 45, you can withdraw from your governmental 457b plan with no penalty. You still pay income tax on the withdrawal because the money was pre-tax, but there is no additional 10% hit.

This distinction matters enormously for people who plan to retire early, change careers, or who face unexpected financial situations before age 59½. The 457b is the more flexible tool.

It also makes the 457b particularly useful for people in careers where early retirement is common, such as firefighters, police officers, and other public safety workers who may leave active duty in their 40s or 50s.

403b vs 457b: Investment Options and Fees

Investment options and fee structures vary significantly by employer and plan provider.

403b plans have historically offered annuity products as their primary investment vehicle. Some older 403b plans still lean heavily on annuities, which carry surrender charges, mortality and expense fees, and limited investment flexibility. These can add 1% or more per year in fees on top of underlying fund expenses. If your plan offers a Roth 403b option, check whether the investment menu includes low-cost index funds.

457b plans typically offer a broader menu of mutual funds and often have more competitive pricing. Government 457b plans in particular tend to be well-structured because they are subject to more oversight and competitive bidding processes.

Before contributing to either plan, review the investment menu available to you. If your 403b plan charges high fees but your 457b plan offers low-cost index funds, that is a real argument for prioritizing the 457b. The math compounds significantly over a 30-year career.

Employer Matching: 403b vs 457b

Employer matching, when available, functions similarly in both plans. Your employer contributes additional money to your account based on a percentage of your own contributions.

One important difference in the 457b: employer contributions count toward the same $24,500 limit. In a 403b or 401(k), the combined employee plus employer limit is much higher (up to $70,000 in 2025 for 403b plans). The 457b’s combined limit is the same as the employee-only limit, so employer matching in a 457b effectively reduces how much of your own money you can contribute within that limit.

This is one reason some advisors suggest prioritizing the 403b up to the employer match first, then maximizing the 457b, then going back to max the 403b.

When Contributing to Both Makes Sense

If you have access to both plans, contributing to both is one of the most powerful retirement savings strategies available to public sector workers.

The combination works because:

- Separate contribution limits let you double your annual tax-deferred savings

- The 457b provides early withdrawal flexibility that the 403b lacks

- You reduce current taxable income across both accounts simultaneously

- You accumulate assets in two separate buckets, giving you tax planning flexibility in retirement

A teacher who maxes both plans for 20 years, starting at age 35, can accumulate a retirement portfolio that would take a private-sector worker significantly longer to match within a single 401(k) limit.

Tracking your contributions and investment performance across both accounts takes some organization, especially if you are balancing other savings vehicles like a Roth IRA alongside them. Tools that help you track financial activity across multiple accounts reduce the friction of managing a multi-account retirement strategy. And for public sector employees in organizations that are modernizing their HR and benefits systems, understanding how workplace platforms and operations tools are evolving is relevant context for how your benefits might be administered going forward.

Quick Comparison: 403b vs 457b

| Feature | 403b Plan | 457b Plan |

|---|---|---|

| Who qualifies | Public/private schools, nonprofits, churches | Government employees, some nonprofit executives |

| 2026 contribution limit | $24,500 | $24,500 |

| Age 50+ catch-up | $8,000 | $8,000 |

| Ages 60-63 catch-up | $11,250 | $11,250 |

| Special catch-up | 15-year service provision | 3-year near-retirement double limit |

| Early withdrawal penalty | 10% before age 59½ | No penalty after leaving employer |

| Combined employer limit | Up to $70,000 | Same as employee-only limit ($24,500) |

| Investment options | Often annuity-heavy | Broader mutual fund menus common |

| Separate from 401(k)/403(b) limit? | Shared with 401(k) | Yes, separate limit |

Key Takeaways

- 403b vs 457b: Both are tax-deferred retirement plans for public sector and nonprofit workers. They operate similarly in terms of tax treatment but differ significantly in who qualifies, early withdrawal rules, and special catch-up provisions.

- What is a 403b plan? A retirement savings account for employees of public schools, nonprofits, and religious organizations. Similar to a 401(k) with an early withdrawal penalty before 59½.

- What is a 457 plan? A deferred compensation retirement account for government employees. No early withdrawal penalty after leaving your employer, regardless of age.

- 2026 contribution limits: $24,500 per plan, with separate limits meaning you can contribute to both independently.

- The 457b’s no-penalty early withdrawal rule makes it uniquely valuable for people planning to retire before age 59½.

- If your employer offers both plans, contributing to each is one of the highest-leverage retirement savings strategies available to you.

- Check investment fees before choosing where to direct contributions. Plan quality varies significantly by employer.