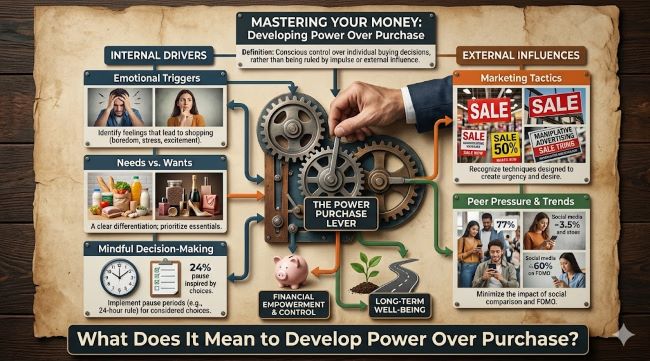

What Does It Mean to Develop Power Over Purchase?

Developing power over purchase is one of the most practical financial skills a person can build, and also one of the least discussed in formal financial education. The concept sits at the intersection of behavioral psychology and personal finance: it describes the ability to make intentional, deliberate spending decisions rather than reactive ones driven by impulse, marketing, social pressure, or emotion. This guide explains what it means to develop power over purchase, why it matters, and how to actually build it.

What Power Over Purchase Means

Power over purchase means being in control of your spending decisions rather than being controlled by them. It’s the capacity to pause between the desire to buy something and the act of buying it, evaluate whether the purchase aligns with your values and financial goals, and make a conscious choice rather than an automatic one.

This doesn’t mean never spending money or avoiding enjoyable purchases. It means the purchases you make are ones you chose deliberately rather than ones that happened to you because of effective marketing, peer pressure, emotional state, or the simple availability of something desirable.

When you develop power over purchase, spending becomes a tool you direct rather than a force that directs you. You determine where your money goes rather than looking at a bank statement at the end of the month wondering where it went.

Why Power Over Purchase Matters Financially

The financial case for developing power over purchase is straightforward: unmanaged impulse spending is one of the most common reasons people fail to reach financial goals despite earning adequate income.

Research on consumer behavior consistently shows that a significant portion of purchasing decisions are made impulsively, without prior planning. Retail environments, e-commerce platforms, and digital advertising are designed specifically to reduce the gap between desire and purchase: one-click buying, limited time offers, “frequently bought together” suggestions, and targeted ads all work to eliminate the pause that gives you the chance to exercise judgment.

Without power over purchase, income is consumed by small, unplanned spending that adds up to significant amounts over a month. With it, the same income can be redirected toward savings goals, debt reduction, or purchases that genuinely matter to you.

The Psychology Behind Impulsive Spending

To develop power over purchase effectively, understanding why impulse buying happens is useful.

Dopamine and instant gratification. The anticipation of a purchase triggers a dopamine response in the brain. This reward signal happens before the purchase, not after: which is why buying something feels good even when the item disappoints afterward. Developing power over purchase involves recognizing this dopamine trigger and not treating the feeling of wanting to buy as a signal that you should buy.

Scarcity and urgency cues. “Only 3 left in stock,” “Sale ends tonight,” and similar messaging exploits loss aversion, the psychological tendency to feel losses more keenly than equivalent gains. These cues create artificial urgency that bypasses deliberate decision-making. When you develop power over purchase, you recognize these tactics and don’t let manufactured urgency drive real spending decisions.

Social comparison and identity spending. Purchases made to maintain social standing, match what peers have, or signal a particular identity are particularly resistant to deliberate evaluation because they’re tied to emotional needs beyond the object itself. Developing power over purchase includes examining whether a desired item reflects genuine personal preference or social pressure.

Emotional spending. Stress, boredom, loneliness, and celebratory moods all trigger spending in different ways. Shopping as emotional regulation is common but costly. Building awareness of your emotional state before purchases is a core component of developing power over purchase.

Practical Strategies to Develop Power Over Purchase

The 24-48 hour rule. For any unplanned purchase above a threshold you set (many people use $50 or $100), wait 24-48 hours before completing the transaction. Most impulse purchases lose their urgency within a day. If after 48 hours you still want the item and it fits your budget, buy it deliberately. If the desire has faded, you’ve exercised power over purchase successfully.

Remove friction-reducing features. Saved payment information, one-click buying, and stored shipping addresses reduce the effort required to complete a purchase. Removing these forces a small amount of friction back into the process, which is enough to interrupt automatic purchasing behavior. Deleting saved card information from retail sites is one of the simplest ways to develop power over purchase.

Shop with a list and stick to it. Whether at a grocery store, a retail store, or an online retailer, knowing exactly what you came to buy and limiting yourself to that list is a direct exercise of purchase power. Anything not on the list gets evaluated deliberately rather than added automatically.

Identify your spending triggers. Track not just what you buy impulsively but when and why. Most people find patterns: late-night browsing, shopping after a stressful day, browsing social media while bored. Recognizing your personal triggers is the first step to interrupting them before the purchase happens.

Create a “want list” instead of buying immediately. When you see something you want, add it to a running list rather than buying it immediately. Review the list weekly or monthly. Some items will have lost their appeal by the time you review. Others will remain genuinely desirable. Buying from the list rather than in the moment shifts the decision from impulse to intention.

Budget a discretionary spending allowance. A budget that leaves no room for personal spending fails because it’s unsustainable. Developing power over purchase is not about eliminating discretionary spending: it’s about making that spending intentional. A defined monthly amount for personal spending that you can use freely within the budget removes guilt from deliberate spending while containing unplanned spending.

Power Over Purchase and Financial Goals

Developing power over purchase is most meaningful when connected to specific financial goals. The clearer your financial priorities — paying off debt, building an emergency fund, saving for a down payment, investing for retirement — the easier it is to evaluate any given purchase against those priorities.

Every spending decision is implicitly a choice about where resources go. When you develop power over purchase, you make that choice explicitly rather than by default. A purchase that competes with a savings goal you care about becomes easier to decline not because of willpower but because of clarity about what matters more.

This goal-connection also makes the practice feel less like deprivation and more like agency. You’re not refusing to buy something because you can’t afford it: you’re choosing not to buy it because something else matters more to you right now. That distinction shifts the psychological experience from scarcity to autonomy.

For related financial skills that complement developing power over purchase, what are some key components of successful budgeting covers the structural framework that gives power over purchase its context: a budget is where your priorities are defined, and purchase power is how you honor them in real time.

Key Takeaways

- Power over purchase means making deliberate, intentional spending decisions rather than reactive ones driven by impulse, emotion, social pressure, or marketing

- The financial impact of unmanaged impulse spending is significant: small unplanned purchases accumulate into large monthly totals that prevent progress toward savings and financial goals

- Understanding the psychology behind impulse spending (dopamine triggers, artificial urgency, social comparison, emotional regulation) makes it easier to recognize and interrupt those patterns

- The 24-48 hour rule is the most effective single practice: waiting before completing any unplanned purchase above a personal threshold eliminates most impulse buys without requiring ongoing willpower

- Removing friction-reducing features (saved card information, one-click buying) from retail sites restores the natural pause that impulse-buying design deliberately eliminates

- A personal “want list” where desired items wait for deliberate review transforms impulse into intention without requiring you to deny all unplanned desires

- Power over purchase is most sustainable when connected to clear financial goals: clarity about what matters more makes declining competing purchases feel like agency rather than deprivation