Why Is It Important to Find a Credit Card with a Lower APR?

Most people choose a credit card based on the rewards program, the sign-up bonus, or the brand name. The APR — annual percentage rate — gets a quick glance and then mostly ignored. That’s a costly mistake for anyone who carries a balance, pays off slowly, or hits a financial rough patch where the balance lingers longer than planned. Understanding why it is important to find a credit card with a lower APR is fundamental to understanding how credit actually costs money.

What APR Is and How It Works

APR stands for annual percentage rate. It represents the yearly cost of borrowing money on your credit card, expressed as a percentage. A card with a 24% APR charges you 24% of your outstanding balance per year in interest.

In practice, credit card interest accrues daily. The daily periodic rate is calculated by dividing the APR by 365. So a 24% APR becomes a daily rate of approximately 0.066%. That daily rate is applied to your outstanding balance each day, and the accumulated interest is added to your balance at the end of each billing cycle.

This is where the compounding effect becomes significant. If you carry a $1,000 balance at 24% APR and make no payments, after one month you owe roughly $20 more. That $20 is now part of your balance, and next month interest is calculated on $1,020. Over time this compounds into a meaningfully larger debt than the original amount borrowed.

Why a Lower APR Directly Reduces What You Pay

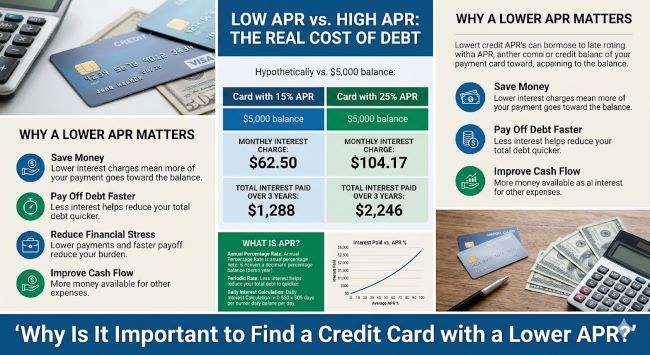

The most straightforward reason why it is important to find a credit card with a lower APR is simple arithmetic: a lower rate means less interest charged on the same balance. The difference is not trivial.

Consider a $3,000 balance on two cards:

- Card A at 29% APR: paying $100 per month, you’d pay approximately $2,400 in interest and take over four years to pay off the balance.

- Card B at 16% APR: paying the same $100 per month, you’d pay roughly $900 in interest and clear the debt in under three years.

Same balance. Same monthly payment. The difference is $1,500 in interest and more than a year of debt simply because of the rate difference. That $1,500 represents money that could have gone to savings, an emergency fund, or investments.

Why APR Matters Even If You Pay in Full Most Months

Some people assume APR doesn’t matter because they typically pay their balance in full each month and therefore pay no interest. This is mostly true in normal circumstances, but several common situations change the calculation:

Unexpected expenses. A medical bill, car repair, or job loss can leave a balance that takes months to pay down. In that moment, the APR you chose when you signed up determines how much that financial stress costs you.

Promotional purchases. Large purchases sometimes get paid off over several months rather than at once. During that stretch, your APR determines the carrying cost.

Deferred interest offers. Some retail credit cards advertise 0% interest for a promotional period, but if any balance remains at the end of that period, interest accrues retroactively at the card’s full APR — often 27% or higher. If that rate is high, a missed payoff is extremely costly.

Transferred balances. If you transfer a balance from one card to another, the APR of the receiving card determines your ongoing cost once any promotional 0% period ends.

The Compounding Interest Problem

Why it is important to find a credit card with a lower APR becomes even clearer when you understand how compounding interest works against you. Credit card interest compounds daily, not annually, which means your effective rate is slightly higher than the stated APR.

More importantly, minimum payments are typically set low enough (often 1-2% of the balance) that a significant portion of each payment goes to interest rather than principal. At high APRs, minimum payments may barely cover the monthly interest charge, leaving the principal almost unchanged month after month.

This is how people end up paying thousands in interest on a few hundred dollars of original spending. The debt doesn’t shrink because the high rate consumes most of each payment before it reaches the principal.

A lower APR means a larger portion of each payment goes toward reducing the actual balance, not just covering interest charges.

APR vs. Rewards: Which Matters More?

Credit card rewards programs are aggressively marketed and easy to value: 2% cash back on every purchase, airline miles, hotel points. These benefits are real and worth having when managed correctly.

But the math on rewards versus APR becomes very unfavorable very quickly for anyone carrying a balance. A 2% cash back card with a 28% APR earns you $20 back on $1,000 of spending. If you carry that $1,000 for a month, you pay $23 in interest. You’ve paid more in interest than you earned in rewards on that single billing cycle.

For cardholders who never carry a balance, rewards matter and APR matters less. For anyone who sometimes carries a balance, even occasionally, a lower APR card almost always produces better financial outcomes than a high-APR rewards card. The interest savings dwarf the reward earnings.

How to Find a Credit Card with a Lower APR

When comparing cards, focus on the purchase APR listed in the Schumer Box — the standardized disclosure box required in credit card marketing materials. Watch for:

Variable vs. fixed APR. Most credit card APRs are variable, tied to the prime rate plus a margin. This means they can rise when the Federal Reserve raises rates.

The APR range for your credit score. Advertised rates are usually given as a range (e.g., 19.99%-29.99% APR). Your actual rate depends on your creditworthiness. A higher credit score typically qualifies you for the lower end of the range.

Penalty APR. Many cards impose a much higher penalty APR (sometimes 29.99% or higher) if you miss a payment. Check the terms for this and what triggers it.

Balance transfer APR. If you’re moving existing debt, the balance transfer rate matters as much as the purchase rate.

Credit unions typically offer lower APR credit cards than major banks. Online comparison tools (NerdWallet, Bankrate, Credit Karma) allow you to filter by APR specifically.

For broader financial context around credit card management, what credit score do you start with covers the starting point of your credit profile, which directly determines the APR range you’ll qualify for when applying for a new card.

Key Takeaways

- APR is the annual cost of borrowing on a credit card: a lower APR means less interest charged on the same balance, which translates directly to money saved

- The difference between a 16% and 29% APR on a $3,000 balance can mean over $1,500 in extra interest payments and more than a year of additional debt on the same monthly payment

- Credit card interest compounds daily: high-APR minimum payments often barely cover the interest charge, leaving principal almost unchanged month to month

- APR matters even if you usually pay in full: unexpected expenses, large purchases, and financial disruptions can leave balances that carry for months at whatever rate you locked in when you applied

- For anyone who carries a balance, APR savings almost always exceed the value of rewards programs: 2% cash back cannot offset 28% interest on the same spending

- Credit unions typically offer lower APR options than major banks: compare using the purchase APR in the Schumer Box, not the teaser rate

- Your credit score determines which end of an APR range you qualify for: building a stronger credit profile is the most reliable way to access lower-rate cards