What Must an Entrepreneur Assume When Starting a Business?

Starting a business is one of the most consequential decisions a person can make financially and professionally. It involves a set of assumptions, responsibilities, and risks that differ fundamentally from employment. Understanding what an entrepreneur must assume when starting a business isn’t just an academic exercise: it’s the realistic foundation that separates entrepreneurs who plan well from those who underestimate what they’re taking on. This guide covers the core assumptions every entrepreneur needs to make from day one.

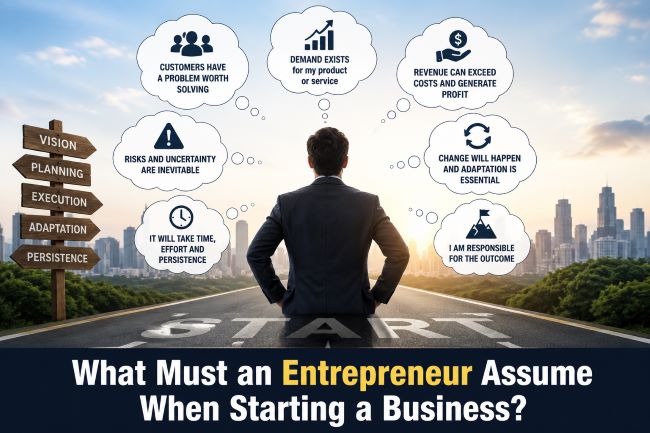

The Central Assumption: Risk

The most fundamental thing an entrepreneur must assume when starting a business is risk. Not risk in a vague sense, but specific, quantifiable forms of it.

Financial risk is the most obvious. The entrepreneur may invest personal savings, take on debt, or give up stable employment income to start the venture. If the business fails, that capital is lost. In many cases, particularly for sole proprietors or small business partnerships without proper legal structures, personal financial liability extends beyond the business itself: personal assets can be at stake depending on the business structure chosen.

Income risk is the corollary. Unlike employment, where income is relatively predictable, an entrepreneur’s income is directly tied to the business’s performance. In the early stages, many entrepreneurs pay themselves little or nothing and reinvest available cash into the business. The expected financial security of a salary is replaced by the uncertain and variable return of a business owner.

Opportunity cost risk is often underestimated. Every year spent building a business is a year not spent in a salaried career, building pension contributions, or pursuing other opportunities. The entrepreneur assumes that the potential upside of the business justifies not just the direct financial risk but the cost of the alternative path not taken.

The Assumption of Uncertainty

An entrepreneur must also assume uncertainty: not just risk (which can sometimes be estimated or hedged) but genuine unknowns that cannot be fully anticipated.

Market uncertainty: will customers actually want what the business is offering? No amount of market research fully eliminates the possibility that the real-world response to a product or service differs from what research suggested.

Competitive uncertainty: will existing competitors respond, and how? Will new competitors enter? Will a technology change make the product less relevant?

Operational uncertainty: will the supply chain hold? Will key employees stay? Will costs remain controllable?

Regulatory uncertainty: will the legal environment for the business change in ways that affect the model?

These uncertainties cannot be eliminated by planning, only managed. An entrepreneur must assume that many things will not go according to plan and that the ability to adapt is as important as the original plan itself.

The Assumption of Full Responsibility

In employment, responsibility is shared and layered. A manager is accountable to their director, who is accountable to a VP, who is accountable to a CEO and board. There are structures above any individual employee that catch some of the consequences of decisions.

An entrepreneur starting a business, particularly in its early stages, assumes full responsibility. When something goes wrong with a customer order, the entrepreneur handles it. When a supplier fails, the entrepreneur finds a solution. When cash flow tightens, the entrepreneur decides what to pay and what to defer. When a legal issue arises, it lands on the entrepreneur’s desk.

This assumption of responsibility extends to areas where the entrepreneur may have no prior expertise: accounting, legal compliance, employment law, marketing, operations, and customer service all require attention even if the entrepreneur’s core skill is in something entirely different. The early-stage entrepreneur either learns these areas, manages contractors and advisors who handle them, or accepts the consequences of neglecting them.

The Assumption of Initial Losses

What an entrepreneur must assume when starting a business includes the likelihood of operating at a loss initially. Most businesses require time to build customer bases, refine their product, establish operational efficiency, and generate enough revenue to cover their costs.

The period before profitability is called the valley of death by startup practitioners: it’s the stretch where expenses are real and revenue is either absent or insufficient, and where many businesses fail not because the core idea was wrong but because they ran out of capital before reaching sustainable operations.

A realistic entrepreneur assumes this period will exist, estimates how long it will last, calculates the capital required to survive it, and secures that capital before launching rather than hoping revenue will arrive faster than expected.

The Assumption of Wearing Many Hats

In a large organization, functions are divided among specialists. There’s a marketing team, a finance team, a legal team, an HR team. A new entrepreneur starting a business assumes that in the early stages, they will perform many or most of these functions themselves.

This assumption matters for time planning: an entrepreneur is not just running the operation they started the business to run. They’re also doing invoicing, handling customer complaints, managing vendor relationships, filing taxes, posting on social media, and any number of tasks peripheral to the core business. The ability to handle this breadth of responsibility, or to recognize quickly which functions need to be delegated and find affordable ways to do so, is a critical entrepreneurial skill.

The Assumption of Long Time Horizons

What an entrepreneur must assume when starting a business includes a realistic time horizon. Most successful businesses take years, not months, to reach meaningful scale or profitability. Research on startup timelines consistently shows that entrepreneurs underestimate the time required to reach key milestones.

This assumption has practical consequences. Personal financial planning, relationship expectations, lifestyle adjustments, and stress management all need to account for a multi-year commitment during which the business may consume most of the entrepreneur’s time and energy without yet providing a market-rate financial return.

Entrepreneurs who assume quick results set themselves up for discouragement and premature abandonment of ventures that would have succeeded with sustained effort. Realistic time horizon assumptions are protective: they set expectations that allow the entrepreneur to stay the course during the inevitable slow periods.

The Assumption of Market Validation Responsibility

A new business enters a market that doesn’t yet recognize it. An entrepreneur must assume the responsibility of proving to the market that their product or service solves a real problem better than existing alternatives. This is not automatic: customers don’t seek out new businesses simply because they exist.

Market validation: demonstrating that real customers will pay real prices for what the business offers, is the entrepreneur’s first critical task. It requires testing, iteration, listening to feedback, and often adjusting the offering significantly from the original concept. The assumption that the market will respond as planned is one of the most dangerous assumptions an entrepreneur can make: the reality is usually different, and the entrepreneur must assume the responsibility of discovering that difference early rather than late.

For broader context on how entrepreneurial ventures compete within market structures, which helps enable an oligopoly to form within a market is a related economic concept that helps entrepreneurs understand the competitive environment they’re entering and what structural advantages incumbents may hold.

Key Takeaways

- The most fundamental thing an entrepreneur must assume when starting a business is risk: financial, income, and opportunity cost risk are all present and must be consciously accepted

- Uncertainty is distinct from risk: entrepreneurs must assume that many things cannot be predicted or planned for, and that adaptability is as important as the business plan

- Full responsibility for all aspects of the business falls on the entrepreneur in the early stages: there is no management layer above to catch consequences of decisions

- Initial losses are a realistic assumption for most new businesses: the period before profitability requires sufficient capital reserves, which must be secured before launch

- Wearing many hats across functions (finance, marketing, operations, legal) is an early-stage reality that requires either personal breadth or affordable delegation

- Realistic time horizons (years, not months) are a necessary assumption: underestimating the time to profitability is a common and costly mistake

- Market validation is the entrepreneur’s responsibility: the market doesn’t automatically recognize or embrace a new business, and discovering this early through testing and iteration is essential