Which Statement Best Describes How an Investor Makes Money Off Debt?

Debt is not just a liability for the borrower: it’s an asset for the investor on the other side of the transaction. Understanding how investors generate returns from debt instruments is fundamental to understanding financial markets, portfolio construction, and why institutional money flows into bonds, loans, and debt-based securities at the scale that it does. This guide explains clearly which statement best describes how an investor makes money off debt and unpacks the mechanics behind each return mechanism.

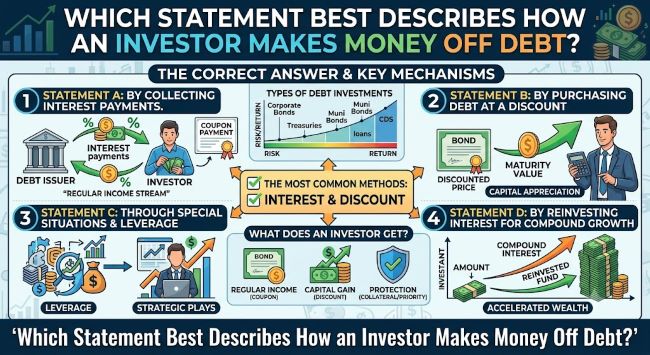

The Core Answer: An Investor Makes Money Off Debt by Earning Interest

The most direct and accurate statement describing how an investor makes money off debt is this: an investor lends money (or buys a debt instrument) and earns a return through the interest payments the borrower makes over the life of the loan or bond, plus the return of the principal at maturity.

This is the foundational mechanism of debt investing. When you buy a corporate bond, a US Treasury, a municipal bond, or when a bank makes a loan, the investor receives periodic interest payments (called coupon payments in the case of bonds) and eventually receives the original principal back when the debt matures. The interest payments represent the price the borrower pays for using the investor’s money and the compensation the investor receives for bearing the risk of lending.

This is what separates debt investing from equity investing. An equity investor (shareholder) makes money through the company’s growth and profits, primarily via price appreciation and dividends. A debt investor makes money through the contractual obligation of the borrower to pay interest and return principal, regardless of how the borrower’s business performs (as long as they don’t default).

The Three Ways Investors Make Money Off Debt

1. Interest Income (Coupon Payments)

Interest income is the primary source of return for most debt investors. When an investor buys a bond with a face value of $1,000 and a 5% annual coupon rate, they receive $50 per year in interest payments (typically paid semi-annually as $25 every six months). At maturity, they receive the $1,000 principal back.

The interest rate on a debt instrument reflects several factors:

Risk premium: higher-risk borrowers pay higher interest rates to compensate investors for the greater probability of default. This is why junk bonds (high-yield bonds issued by companies with weak credit ratings) pay more than investment-grade corporate bonds, which pay more than US Treasuries (considered risk-free).

Duration premium: longer-term debt generally pays higher interest than shorter-term debt because investors are locking up their money for longer and face more uncertainty over a longer period.

Inflation expectation: interest rates incorporate expected inflation because investors need to earn a return above the inflation rate to maintain purchasing power.

2. Price Appreciation (Capital Gains)

Investors can also make money off debt through price appreciation: buying a bond at a discount and selling it at a higher price before maturity, or benefiting from interest rate changes.

Bond prices and interest rates move inversely. When interest rates fall, existing bonds paying higher fixed coupon rates become more valuable relative to newly issued bonds (which pay the new, lower rates). A bond purchased at par ($1,000) when rates were 5% may be worth $1,100 if rates fall to 3%, because the 5% coupon is now worth more in a lower-rate environment.

Investors who anticipated the rate decline and bought bonds before it happened can sell those bonds at a profit. This is how professional bond fund managers generate returns beyond just coupon income: actively managing duration and positioning to benefit from rate movements.

Conversely, when interest rates rise (as during contractionary monetary policy), bond prices fall and investors who need to sell before maturity can experience capital losses.

3. Distressed Debt and Spread Compression

A more sophisticated way investors make money off debt involves buying distressed or below-investment-grade debt at a significant discount to face value. If a company’s bonds trade at 50 cents on the dollar because the market fears default, an investor who correctly assesses that the company will recover can buy those bonds and earn a large return when the bonds trade back toward par value.

Hedge funds and private credit investors specialize in this approach, buying debt of companies in financial difficulty, sometimes participating in restructuring, and earning returns both from interest and from price recovery as the company’s situation improves.

Debt Instruments Investors Use

Understanding how an investor makes money off debt becomes clearer when you look at the range of instruments that exist:

Government bonds (Treasuries, gilts, bunds): the lowest-risk debt instruments, paying lower interest in exchange for near-zero default risk. Investors use these for safety and liquidity.

Corporate bonds: issued by companies, paying higher interest than government bonds to compensate for default risk. Range from investment-grade (strong companies) to high-yield or junk (weaker credit profiles).

Municipal bonds: issued by state and local governments in the US, often with tax-advantaged interest for investors in high tax brackets.

Mortgage-backed securities (MBS): pools of mortgages packaged into a security. Investors receive interest and principal payments from the underlying mortgage borrowers. This is how institutional investors participate in the mortgage market.

Collateralized Loan Obligations (CLOs): pools of corporate loans packaged into tranches with different risk-return profiles. The riskiest tranches earn the highest interest but absorb losses first.

Peer-to-peer loans and private credit: direct lending by investors to individuals or businesses through platforms or private funds. Higher interest rates reflect the higher risk and lower liquidity compared to publicly traded bonds.

The Risk-Return Relationship in Debt Investing

Which statement best describes how an investor makes money off debt must also account for risk. An investor doesn’t just make money off debt: they make money in exchange for bearing certain risks, primarily:

Default risk: the borrower doesn’t pay back the interest or principal. Higher default risk commands higher interest rates.

Interest rate risk: rising rates reduce the market value of existing fixed-rate bonds.

Inflation risk: if inflation exceeds the interest rate earned, the investor loses purchasing power in real terms.

Liquidity risk: some debt instruments (private loans, certain corporate bonds) can’t be easily sold before maturity, requiring a liquidity premium in the interest rate.

The interest rate an investor earns is compensation for all of these risks simultaneously. A higher rate signals higher risk: the investor who earns 9% on a high-yield bond is being compensated for a much higher probability of loss than the investor earning 4% on a Treasury bond.

For context on how interest rates connect to broader economic policy, which best explains how contractionary policies can hamper economic growth covers how central bank rate decisions flow through the economy and directly affect the debt markets where investors earn their returns.

Key Takeaways

- The best statement describing how an investor makes money off debt: an investor lends capital and earns a return through contractual interest payments over the life of the debt plus the return of principal at maturity

- Interest income (coupon payments) is the primary return mechanism: the interest rate reflects risk premium, duration premium, and inflation expectations

- Price appreciation is the secondary mechanism: bond prices rise when interest rates fall, allowing investors who sell before maturity to earn capital gains beyond coupon income

- Distressed debt investing generates returns by buying bonds or loans at a discount to face value and profiting as the borrower’s financial situation improves

- Debt instruments range from near-risk-free government bonds (low interest) to high-yield corporate bonds and private credit (high interest) to distressed debt (potential large returns with high default risk)

- The interest rate an investor earns is compensation for default risk, interest rate risk, inflation risk, and liquidity risk simultaneously: higher rates always signal higher underlying risk

- Unlike equity investors who depend on company growth, debt investors earn through contractual obligation: they have legal priority over equity holders in a default scenario