What Type of Tax Is Used as Income by Retired People and People with Disabilities?

The answer to this question is one of the most important concepts in understanding how the American social safety net is funded. The type of tax that serves as income for retired people and people with disabilities is the payroll tax, specifically the Social Security payroll tax collected under the Federal Insurance Contributions Act (FICA). This guide explains what payroll taxes are, how they become the income that retirees and disabled people receive, how the system works, and what you need to know about it.

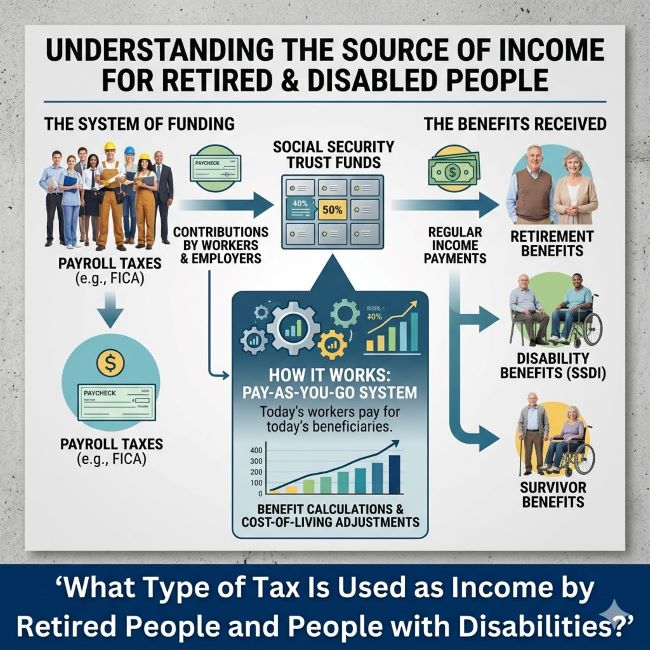

The Direct Answer: Payroll Taxes (FICA)

Payroll taxes are taxes withheld from workers’ paychecks and matched by employers, with the proceeds funding Social Security and Medicare. The Social Security portion of payroll tax is the specific tax that becomes income for retired people and people with disabilities.

Every paycheck you receive has two Social Security-related deductions:

Social Security tax: 6.2% of wages up to the Social Security wage base ($168,600 in 2024). Your employer matches this with another 6.2%, for a combined 12.4% contribution on your wages.

Medicare tax: 1.45% of all wages, also matched by your employer for a combined 2.9%. An additional 0.9% Medicare surtax applies to high earners above $200,000 ($250,000 for married filing jointly) but this is not matched by employers.

For self-employed workers, the self-employment tax covers both the employee and employer portions: 12.4% for Social Security and 2.9% for Medicare, for a total of 15.3% on net self-employment income.

How Payroll Taxes Become Retirement and Disability Income

The Social Security portion of payroll taxes flows into two trust funds administered by the Social Security Administration (SSA):

Old Age and Survivors Insurance (OASI) Trust Fund: funds monthly benefits for retired workers and their dependents, as well as survivors of deceased workers.

Disability Insurance (DI) Trust Fund: funds monthly benefits for workers who become disabled and are unable to work, as well as their dependents.

Current workers’ payroll tax payments fund current beneficiaries’ checks. This is the pay-as-you-go structure of Social Security: it is not a personal savings account where your specific contributions accumulate for your own future use. Rather, the taxes paid by today’s workforce support today’s retirees and disabled workers, and tomorrow’s workforce will support the people who are working today.

This structure is why the ratio of workers to beneficiaries matters for Social Security’s financial health. In 1960 there were approximately 5 workers for every Social Security beneficiary. Today that ratio is closer to 2.7 workers per beneficiary, and it’s projected to continue declining as the population ages.

Social Security Retirement Benefits

Retired workers become eligible for Social Security benefits based on their work record and the payroll taxes paid over their career.

Eligibility: workers need 40 credits (generally equivalent to 10 years of work) to qualify for retirement benefits.

Benefit amount: calculated based on your average indexed monthly earnings (AIME) during your 35 highest-earning years. The formula is progressive: it replaces a higher percentage of income for lower earners than for higher earners.

Claiming age: benefits can be claimed as early as age 62 (reduced benefit) or as late as age 70 (maximum benefit). Full retirement age for people born after 1960 is 67. Each year you delay claiming beyond full retirement age increases your benefit by 8% per year until 70.

The benefit you receive as a retiree is funded by the payroll taxes being paid by workers at that moment, which is why payroll tax is accurately described as the type of tax that serves as income for retired people.

Social Security Disability Benefits (SSDI)

Social Security Disability Insurance (SSDI) is funded by the same payroll taxes through the DI Trust Fund. It provides monthly income to workers who become unable to work due to a qualifying disability.

Eligibility: a worker must have a medical condition meeting SSA’s definition of disability (inability to do substantial gainful activity for at least 12 months due to a medical condition) and must have sufficient recent work history. Generally, the worker needs 20 credits earned in the last 10 years before becoming disabled.

Benefit amount: calculated similarly to retirement benefits, based on the worker’s earnings history. The average SSDI benefit in 2024 is approximately $1,537 per month.

Medicare: SSDI recipients become eligible for Medicare after a 24-month waiting period, funded by the Medicare payroll tax.

Supplemental Security Income (SSI): A Different Funding Source

It’s important to distinguish SSDI from Supplemental Security Income (SSI), which also provides income to disabled people (and elderly people with very low income) but is funded differently.

SSI is funded through general federal revenues (income taxes), not payroll taxes. It’s a needs-based program with no work history requirement. The payroll tax connection applies specifically to SSDI (and Social Security retirement), not to SSI.

This distinction answers a nuance in the original question: the payroll tax serves as income for retired people (through Social Security retirement) and people with disabilities who have sufficient work history (through SSDI). People with disabilities who lack sufficient work history may receive SSI, which comes from general tax revenues rather than payroll taxes.

Why This Structure Matters

The payroll tax funding mechanism for Social Security was deliberately designed to create a contributory relationship: workers earn benefits by contributing to the system throughout their working lives. This design has historically given Social Security strong political durability because beneficiaries are receiving something they “paid into” rather than a welfare benefit.

The funding structure also creates a direct link between economic activity and Social Security’s income. When employment is high and wages are rising, payroll tax revenue increases. When unemployment rises, payroll tax revenue falls just as benefit claims (particularly SSDI claims) may rise, creating pressure on the trust funds.

For related financial planning context, understanding how payroll taxes fund your future retirement income connects to what are some key components of successful budgeting, since Social Security benefit projections are an important input to retirement budget planning.

Key Takeaways

- The type of tax used as income by retired people and people with disabilities is the payroll tax, specifically the Social Security portion collected under FICA

- Workers contribute 6.2% of wages to Social Security (up to the annual wage base), matched by employers for a combined 12.4%; self-employed workers pay both portions at 12.4%

- Payroll taxes flow into two Social Security trust funds: Old Age and Survivors Insurance (OASI) for retirees and survivors, and Disability Insurance (DI) for disabled workers

- Social Security operates as a pay-as-you-go system: current workers’ payroll taxes fund current beneficiaries’ checks rather than accumulating in personal accounts

- Social Security retirement benefits are based on your highest 35 earning years and the payroll taxes paid during that time: eligibility requires 40 work credits (approximately 10 years of work)

- SSDI (Social Security Disability Insurance) is funded by payroll taxes and requires a work history; SSI (Supplemental Security Income) is funded by general federal revenues and has no work history requirement

- The declining ratio of workers to beneficiaries (from ~5:1 in 1960 to ~2.7:1 today) is the central long-term financial challenge for payroll tax-funded Social Security

")